Project Report For PMEGP Loan

Get a professionally prepared PMEGP loan project report aligned with the latest bank, KVIC, and MSME guidelines—starting at ₹2,999, delivered in 24–48 working hours. Our bankable DPR includes a detailed business plan, project cost, means of finance, five-year financial projections, profitability analysis, and employment generation details to improve PMEGP loan approval chances and ensure smooth bank processing.

Get free Sample

Introduction

Getting a PMEGP loan approved from a bank largely depends on the quality of your PMEGP loan project report. A professionally prepared, bankable project report clearly explains your business idea, project cost, profitability, and eligibility for government subsidy. Under the Prime Minister’s Employment Generation Programme (PMEGP), entrepreneurs can avail a credit-linked subsidy of 15% to 35% of the total project cost, provided the report is prepared strictly as per KVIC, MSME Ministry, and bank norms.

At Sharda Associates, we specialize in preparing PMEGP Loan Project Reports that are accepted by banks and KVIC, helping applicants get faster loan approval and maximum subsidy benefits.

What is PMEGP?

PMEGP (Prime Minister’s Employment Generation Programme) is a credit-linked capital subsidy scheme administered by KVIC (Khadi and Village Industries Commission) under the Ministry of Micro, Small and Medium Enterprises (MoMSME), Government of India. It was launched in 2008 by merging the Prime Minister’s Rojgar Yojana (PMRY) and Rural Employment Generation Programme (REGP) into a single scheme with significantly enhanced subsidy levels.

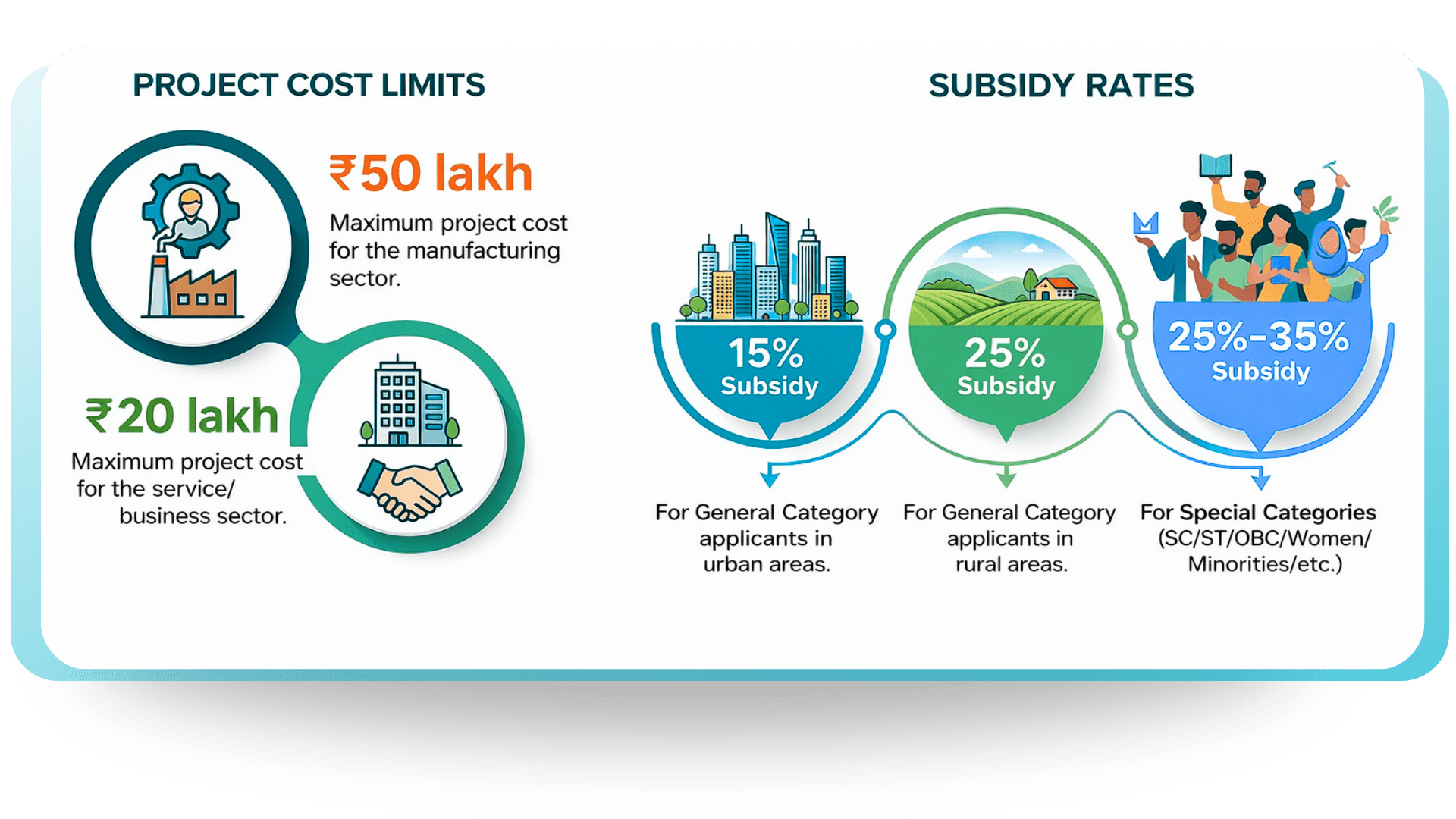

Under PMEGP, eligible entrepreneurs can set up new manufacturing businesses with a project cost of up to ₹50 lakh or new service/trading businesses with a project cost of up to ₹20 lakh. The scheme provides a capital subsidy that is credited to the loan account—effectively reducing the entrepreneur’s debt burden by 15% to 35% of the project cost depending on their category and location.

The scheme is implemented through three nodal agencies: KVIC (Khadi and Village Industries Commission), KVIB (Khadi and Village Industries Boards at the state level), and DIC (District Industries Centres). Applicants apply online through the KVIC portal and select their preferred nodal agency, which then routes the application to a bank branch for loan appraisal.

PMEGP Project Report Format

A PMEGP-compliant project report must be prepared in a bank-acceptable format and include:

- Executive summary of the business

- Promoter profile & background

- Detailed business model

- Project cost & means of finance

- Plant & machinery details

- Working capital assessment

- Market analysis & demand potential

- Manufacturing or service process

- Financial projections (5 years)

- Profit & loss statement

- Cash flow statement

- Break-even analysis

- Employment generation details

- Subsidy calculation as per PMEGP norms

Important: Any mismatch in cost, subsidy percentage, or financials can lead to rejection or delay.

Eligibility Criteria of PMEGP Loan

To apply for a PMEGP loan, the applicant must meet the following eligibility conditions:

- Age should be 18 years or above

- Only new projects are eligible (existing units not allowed)

- Applicant must have passed minimum 8th standard (for projects above ₹10 lakh in manufacturing and ₹5 lakh in services)

- Self-Help Groups (SHGs), Institutions, and Trusts are eligible

- No prior PMEGP subsidy should have been availed

The following entities can apply for a PMEGP loan:

- Individual entrepreneurs

- Proprietorship firms

- Self-Help Groups (SHGs)

- Cooperative societies

- Trusts and registered institutions

Eligible Entities Under PMEGP Scheme

PMEGP Project Cost & Subsidy Calculation

Documents Required for PMEGP Loan

To apply for a PMEGP loan, the applicant must meet the following eligibility conditions:

- Age should be 18 years or above

- Only new projects are eligible (existing units not allowed)

- Applicant must have passed minimum 8th standard (for projects above ₹10 lakh in manufacturing and ₹5 lakh in services)

- Self-Help Groups (SHGs), Institutions, and Trusts are eligible

- No prior PMEGP subsidy should have been availed

Generate Your PMEGP Project Report In Just 3 steps

Connect With Us

Step 01

Share Your Details

Step 02

Get Your Report

Step 03

Step-by-Step PMEGP Application Process

The PMEGP application process begins on the KVIC portal at kviconline.gov.in. Applicants first register on the portal with their basic details and OTP verification. They then fill the online application form—covering personal details, educational qualifications, business plan, and bank preference — and upload the project report, identity documents, educational certificate, caste certificate (if applicable), and any other required supporting documents.

After submission, the application is forwarded to the selected nodal agency (KVIC/KVIB/DIC) for verification and forwarding to the bank. The bank then conducts its credit appraisal of the project report. If the bank is satisfied with the financials and the project is viable, it sanctions the loan. The promoter must deposit their contribution before disbursement. The bank then disburses the loan and separately credits the subsidy amount to a TDR account.

The entire process — from application to loan disbursement — typically takes 3 to 6 months. The timeline varies by state, bank, and DIC processing speed. Active follow-up at each stage significantly accelerates the process.

Why PMEGP Applications Fail — And How to Avoid Rejection

The most preventable reasons for PMEGP rejection are: project report not in KVIC format, employment generation figures too low or not justified in the report, machinery quotations missing from unauthorized or unknown suppliers, unrealistic or inflated financial projections, ineligible applicant (existing business disguised as new), and duplicate applications filed by the same person at multiple banks.

Less commonly, applications are rejected because the proposed business activity is in PMEGP’s negative list — which includes industries considered ecologically harmful, politically sensitive, or in violation of other government policies. Sharda Associates checks the negative list as part of our eligibility assessment before beginning any PMEGP project report preparation.

FAQ's

Banks usually reject PMEGP loan applications due to an improper or non-compliant project report. Common rejection reasons include:

- Project cost not aligned with PMEGP limits

- Incorrect subsidy calculation as per category or area

- Unrealistic profit projections

- Mismatch between machinery quotations and project cost

- Missing employment generation details

A bankable PMEGP project report prepared as per KVIC and MSME guidelines significantly reduces rejection risk.

A PMEGP-compliant project report must clearly explain the commercial viability of the business. It should include:

- Business overview and promoter background

- Detailed project cost (machinery, working capital, infrastructure)

- Means of finance (bank loan, subsidy, own contribution)

- PMEGP subsidy calculation (15%–35%)

- Five-year financial projections

- Profit & loss statement and cash flow analysis

- Break-even point calculation

- Employment generation details

Without these elements, banks cannot complete appraisals.

Yes. If the project report does not follow PMEGP norms:

- Subsidy release may be delayed

- Margin money may not be adjusted by the bank

- KVIC or DIC may raise objections

A properly structured PMEGP project report ensures smooth and timely subsidy adjustment.

To prepare a Detailed Project Report (DPR), you need basic identity proofs, business documents, and financial details. Banks usually ask for Aadhaar, PAN, address proof, Udyam or GST registration, and partnership/company documents if applicable. You also need recent bank statements, past ITRs (if available), and financials for existing businesses. For the project part, you must share machinery quotations, project cost details, raw material information, and production capacity. Along with this, a clear business model, market details, revenue plan, and working capital requirement are needed so a complete, bank-ready DPR can be prepared.

Practically, no. PMEGP guidelines are technical and frequently updated. Even small errors in:

- Financial calculations

- Subsidy percentage

- Cost breakup

can lead to rejection or delays. Most applicants prefer experienced PMEGP consultants for higher approval chances.

Yes. Professional PMEGP consultants usually provide:

- Bank query resolution support

- Financial or cost revisions if required

- Subsidy-related clarifications

- Re-submission assistance

This post-submission support helps speed up loan approval.

If applicant details are clear:

- Service-based projects: 2–3 working days

- Manufacturing projects: 3–5 working days

Delays usually occur due to incomplete documents or unclear cost planning.

Sharda Associates prepares PMEGP project reports that are:

- Fully compliant with bank and KVIC norms

- Customized for each business and applicant

- Based on realistic financial assumptions

- Supported with accurate subsidy calculations

- Backed by post-submission bank assistance

This structured approach results in a higher approval and subsidy success rate.