All about Trust Registration

People establish trusts to give another person control over a portion of their assets or real estate. A trust is created with another person’s interests in mind. The connection between the trustor, trustee, and beneficiary is more fiduciary in nature. As a result, a discrepancy party may be requested as a sort of legal document when an application is going through the trust registration procedure.

A trust is a particular asset or piece of property that is given from the trustor to the trustee with the intention of long-term benefit to the beneficiary. A third party, the beneficiary, may or may not be connected to the trustor and trustee.

As a result, the connection that binds the parties to the trust is critical in defining trust. The Indian Trusts Act of 1882 defines trust as a long-term connection between the trustor and the trustee with the goal of providing a specific benefit to the beneficiary.

What is Trust in an Indian Context?

The Indian Trust Act 1882 governs all registered trusts in India, which streamlines the legal regulations. The Trust is occasionally referred to as a legal structure in which the Trustee obtains property from the Trust’s owner (aka beneficiary). The article of trust ensures that the Trustor’s assets are transferred to the beneficiaries in line with the conditions of the trust agreement.

When the Trust is about to expire, the grantor appoints a trustee to oversee the Trust and finally distribute the grantor’s assets to the specified beneficiaries. Beneficiaries of the Trust in India include heirs, family members, and charity.

Trusts will be used to reduce taxes, simplify or avoid the probate procedure, and protect assets.

There are various kinds of Trust in India, such as;

- Revocable

- Testamentary

- Irrevocable

- Charitable

- Asset protection

- Spendthrift

- Special needs

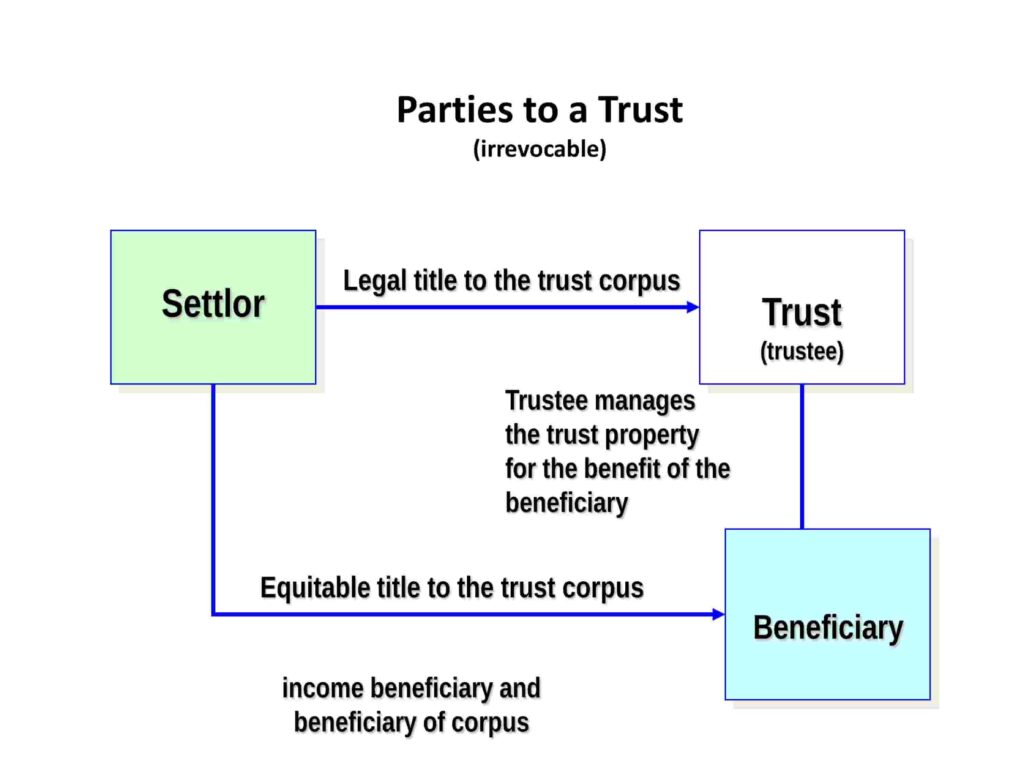

Parties during a Trust

- Author/Settlor/Trustor/Donor: The individual who desires to transfer his property and entrust his trust in another must first create the trust.

- Trustee: Whoever accepts arrogance for the sake of building trust

- Beneficiary: The one who will benefit from the trust in the near future.

Who can create Trust?

A trust is also created by:

- A private, AOP, HUF, corporation, or any other individual who is competent in contracts.

- The consent of a Principal Civil Court of Original Jurisdiction is necessary if a trust is to be established on behalf of a minor.

Furthermore, the extent to which the author of the trust may be able to get rid of his property is dependent on the legal good that is in effect at the time.

What are the categories of Trusts?

There are Four kinds of trusts in India:

- Public Trust

- Private Trust

- Public Cum-Private Trust

- A Company formed under Section 8 of the businesses Act (2013)

Private trusts are governed by the Indian Trusts Act of 1882, whilst public trusts are divided into religious and benevolent trusts. The Religious Endowments Act of 1863, the Charitable and Non-Secular Trust Act of 1920, and the Bombay Trust Act of 1950 are all key laws in India for enforcing public trusts.

Private Trust

A private trust is a legal entity created for the advantage of individuals rather than for the benefit of the public or philanthropic good. It was created to assist one or more beneficiaries known to the Trustor financially. A Private Trust’s benefits are solely available to selected beneficiaries and serve no charitable purpose. Such trusts will most certainly be governed under the Indian Trusts Act of 1882.

Public Trust

The primary goal of a charitable trust is to help the general public. Unlike private trusts, public trusts are not supervised by the Indian Trusts Act and are created for charitable or religious reasons. For the time being, a Trust of this nature follows the general law. Inter Vivos trusts, like private trusts, can be formed by will.

Public-Cum-Private Trusts

The Public-Cum-Private Trusts provide a twofold purpose, as their name suggests. They have the option of using their revenues for both public and private purposes. The beneficiaries of the Trust might be public or private people or both.

A Company formed under Section 8 of the businesses Act (2013)

Private limited companies are governed by Section 8 of the Business Act. On the other side, these businesses are unable to make a profit. Education, crafts, science, the arts, sustainable development, and environmental activities are among the purposes of the enterprises formed as a consequence of this.

Why Trust Registration Process is Required?

Trusts are created with the sole intent of encouraging non-commercial activities. These activities must be field-based, fostering growth in the fields of arts, science, education, and therefore the environment. As a result, establishing a trust is critical. The following advantages can be acquired by establishing a trust in India.

- To guarantee that all activities performed on behalf of the trust are appropriately controlled.

- Develop and encourage initiatives that will lead to a far better society.

- To claim revenue enhancement advantages under 12A and 80 G, you must first register as a trust.

- Beneficiaries in the event of a trust are the general public. To advance the event of trust, every trust must work in the best interests of the general public.

- This licence is essential in order for trust firms to operate legally.

- To improve diverse societal areas.

Who regulates Trust Registration?

The primary regulatory agency for trust registration is the Registrar of Trusts. The registrar of trusts maintains all the data on the trusts which are registered in India. The Trusts Act, 1882 governs registrations of personal Trusts.

No law governs the registration of trusts. Separate state acts apply to trusts registered in multiple states, which the applicant must be aware of. The Bombay Trust Act governs the registration of trusts in Bombay. In India, public trusts must be registered with the appropriate state authorities (if required).

The following laws regulate trusts:

- Trusts Act, 1882

- Income Tax Act, 1961

- Societies Registration Act, 1860.

What are the advantages of Trust Registration?

To Involve In Charitable Undertakings

Public trust is primarily how to line up your assets to learn you, concerned beneficiaries, & a charity simultaneously. A trust like this could provide several benefits to someone looking to help society with non-essential assets like stocks or real estate.

Accessibility to Tax Exemptions

The Income-tax department provides several tax breaks to all registered trusts in India. Because, unlike NGOs, the Trust’s mission does not revolve around profit generation, they are entitled to a variety of tax breaks. However, such an advantage is only available to trusts that have a registered deed on hand.

Trusts are very useful for obtaining capital and income tax benefits. The Trust may offer stronger protection to the settlor, beneficiaries, and trust assets from more stringent tax regulations.

Provide Benefits to Financially Aggrieved Individual

The registered Trust provides much-needed assistance to the disadvantaged and the general public through charity initiatives.

Encounter Minimal Legal Hindrances

The 1882 Indian Trusts Act gives the Trust a lot of legal protection. It also prohibits any third party from filing a baseless claim that could harm Trust’s legal position.

Ensures Legal Coverage for the Family Wealth

Trust is often accustomed allocate specific assets like land/interest within the entity formed by the family, which otherwise wouldn’t be practical for a trustor to separate between individuals.

Avert tribunal

Anybody can leverage trust registration as a tool for transferring an asset to the heir within the absence of a Will. because the legal title of the assets transfers from the settlor to the Trustee within the case after they are “settled”, there’s no change of ownership after settlor demise, thus evading the necessity for probate of a will on account of trust assets.

Unlike probate, the trust acts as a non-public agreement that skips the necessity for added registration. the utilization of a trust may also avert the economic adversity often encountered by a surviving spouse while awaiting a grant of probate.

Immigration/Emigration of Family

When a private & her/his family move to a different nation, it’s an ideal event to determine a trust to induce obviate taxation within the destination country, thereby safeguarding the family assets and facilitating flexibility in its organization.

Eligibility Criteria for Trust Registration

The following criteria would apply to trust registration:

- There must be a minimum of two or more persons for forming the trusts.

- The trust must be formed in keeping with the provisions of the Indian Trusts Act, 1882.

- The parties must not be disqualified under any law operative in India.

- The objectives of the trust must not go against any law operative in India.

- The trustee’s actions must be consistent with the law.

- The formation of the trust must not go against the public interest or the other law effective

- Any trust activities must not injure someone.

- The activities conducted by the trust must not go in keeping with the memorandum.

- Trust Deed must be properly drafted and intend the 000 interests of the parties forming the trust.

- If there are over two purposes of making trust, then both the needs must be valid. If one object is valid and another object is invalid, then the trust can’t be formed.

Fundamental Documentation Required for Trust Registration

Following are key documents that one has to arrange for trust registration:

- Proof associated with Identity for Trustor & Trustee like Aadhaar Card, Voter ID, Passport, DL

- Address Proof associated with Registered Office like Copy of Certificate of Property/Utility Bills

- No objection certification from the owner of the property is rented.

- Trust deed’s objective

- Detail about the Trustee and settlor like Self-attested copy Id & Address Proof and occupation

- Trust Deed on Proper Stamp Value

- Trustee and settlor Photos

- Trustee and settlor

- PAN details

- Trust deed must reflect the subsequent information:

- Number of trustees

- Trust registered address

- Proposed name of the trust

- Proposed Rules that may govern the trust

- Presence of the settlor in addition to two witnesses at the time of registration of Trust

Step-by-Step Procedure for Registering a Trust in India

The following are the steps in the detailed procedure for trust registration:

Step 1: Select an Apt Name for the Trust

The first and foremost step within the process of Trust registration is the name selection for the proposed Trust. Be mindful while serving such a purpose and take the subsequent points under consideration to avoid any hassles:

- The name should adhere to the Emblems and Names Act of 1950.

- There should be no violation whatsoever when it involves Trademark Act.

- The name should stay original.

Step 2: Drafting of the deed of trust

The instrument’s drafting is critical since it is the only item that makes the Trust legally enforceable.

In general, the following clauses are consolidated in the legal document:

Objects

The Object clause reflects the article behind the formation of the Trust

Acceptance of Funds

This section authorises the Trust to accept cash, immovable property, and subscriptions in the form of contributions, donations, and subscriptions from any individual, government institution, or charitable source. Per the requirement, any donations that interfere with the Trust’s goal are prohibited.

Investments: The investment clause specifies the parameters under which the Trust’s fund shall be lawfully and effectively managed. In addition, this part provided conditions for the optimal deployment of extra funds that appear to be underutilised and will assist in the development of additional revenue through investment.

Power of the Trustees

This specific clause discusses the trustees’ obligations, as the name implies.

Generally, such clauses confer the subsequent powers to the trustees.

- Appointing employee(s)

- Alienating the trust properties

- Opening the checking account within the Trust’s name

- Suing defaulters just in case of legal dispute on behalf of the Trust

- Accepting any gift or donation from a legitimate person or source

- Investing additional funding in securities

Accounts and Audit

This section requires the trustees to keep track of the book of account on a daily basis. It also establishes the need for account auditing, which must be performed by a certified CA.

Winding Up

When all of the Trust’s properties/assets are legitimately handed to the beneficiaries or a similar body, either directly or by resettlement, the trust becomes tense. When the Trust is triggered, the parties concerned must specify any tax obligations incurred as a result of the asset transfer. Furthermore, this paragraph mandates that such a legal obligation be carried out with the consent of the charity commissioner/Court/any other legislation in order to avoid any legal disputes.

Penalties for violating Compliances of Trust Registration

Civil and Criminal Penalties

Defaulters who violate the legal document’s terms face both civil and criminal sanctions. Sections 405 to 409 of the IPC 1860 dealt with the provisions relating to criminal breach of trust.

Application for write-down Account Number

The Trustor Institution must submit an official request to the Assessing Officer for the issuance of a tax write-off account number soon after being registered. For this, Trust can utilise form-49B, which is issued by the IT department. The write-down Account Number shall be included on all challans for payment of amount u/s 200 and TDS certificate, as well as returns delivered u/s 206, 206A, and 206B.

Section 272BB discusses the penalty imposed on the Trust if it fails to get the write-off Account Number. The above-mentioned clause charges a Rs 10,000 penalty in the aforementioned conditions.

Failure to Furnish the Return of Income

Failure to assist in the repatriation of revenue is punishable under the Act. If the TDS certificate was not filed with the return of income due to the taxpayer’s failure to furnish one, the return of income will not be invalidated. This certificate must be provided within two years of the conclusion of the assessment year.

Role of Section 12AB on the Registered Trusts

Ensuring continuous exemption under Sections 10 or 100, all active existing trusts or institutions are needed to acquire fresh registration under Section 12AB, which are registered under the provided sections.

- Section 12A

- Section 12AA

- Section 10(23C)

- Section 80G

Trusts registered under section 10 (23C) or 12AA must also renew their registration under section 12AB. Section 12AA, which describes the procedure for registering trusts or institutions, shall be repealed, and Section 12AB will take effect as soon as the specified period ends, whichever occurs first.