In this post we will learn how to calculate the Quick ratio or Acid-Test ratio with an easy example.

It is a liquidity ratio that determines whether a business’s short-term assets are adequate to meet its current liabilities. In other terms, the quick ratio measures a business’s ability to meet its short-term financial commitments. This article will walk you through the steps of calculating the ratio and discussing its consequences.

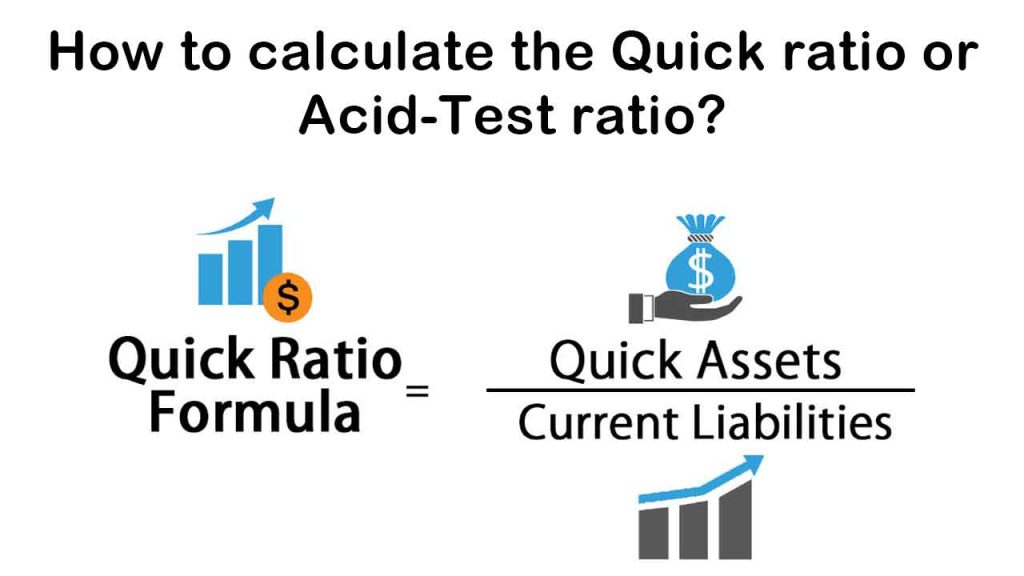

Quick Ratio Formula

Quick Ratio = Current Assets – Inventories – Prepaids/Current Liabilities

Or,

Quick Ratio = Cash + Cash Equivalents + Marketable Securities + Accounts Receivable / Current Liabilities

Important terms –

Cash and cash equivalents – It refers to some of the most liquid current assets on a business’s balance sheet like savings accounts, term deposits with maturities of less than three months, and T-bills.

Marketable securities – These are liquid financial instruments which can be turned into money easily.

Accounts receivables – These are the cash owed to the business as a result of delivering products and/or services to consumers.

Current liabilities – There are loans or liabilities that are due within a year.

Current assets – There are assets which can be turned into cash in less than a year.

Inventories – The price of products and supplies owned by a business with the purpose of selling it to consumers is called inventories.

How to calculate Quick Ratio?

Let calculate quick ratio using a simple example –

Suppose in the balance sheet (in cr) of Airtel Pvt Ltd. For FY 2019, the company shows its Current Assets as 100, Inventories as 25, Prepaids of 5 and Current liabilities of 35. Calculate its quick ratio

Using QR = Current Assets – Inventories – Prepaids/Current Liabilities

Quick ratio = 100-25-5 / 35 = 2

So, quick ratio is 2:1

The quick ratio measures a business’s potential to cover off its current liabilities without selling assets or acquiring new funding. Inventory is excluded from the calculation because it is not often a commodity which can be readily and efficiently turned into currency. The quick ratio is considered a much more optimistic estimate of a company’s financial stability than the current ratio, a liquidity or debt ratio that includes inventory valuation in the calculation.

The higher the percentage, the healthier the business’s liquidity and financial stability. A ratio of 2 indicates that the corporation has $2 in net assets for every $1 in current liabilities. It is crucial to understand, though, that an exceptionally high quick ratio also isn’t deemed desirable as it could mean that the business has surplus cash which is not being properly used to expand its business. A very high ratio can also mean that the business’s accounts receivable are excessively high – this may show collection issues.