Project Report for Mudra Loan — CA Certified, Accepted by All Banks

A Mudra loan application rarely reaches the sanction stage without a well-prepared project report. Under Pradhan Mantri Mudra Yojana, banks and NBFCs use the project report to assess business viability, income projection, cash flow, and repayment capacity. Without it the loan officer has no reason to recommend approval. CA Certified Mudra Loan Project Reports for Shishu, Kishor & Tarun Category by Sharda Associates, Accepted by All Participating Banks & NBFCs in India Starting at ₹2,999 Delivered in 24 to 48 Working Hours

What Is a Mudra Loan?

Mudra Loan is a government– The Pradhan Mantri Mudra Yojana (PMMY) is a government-backed business loan scheme providing financing access to micro and small non-corporate, non-farm enterprises. Mudra loans are offered by public sector banks, private banks, NBFCs, and microfinance institutions (MFIs).

Mudra loans are primarily used for working capital requirements, equipment purchase, shop setup, small manufacturing unit establishment, and service-based business funding.

Three categories under PMMY:

- Shishu — Up to ₹50,000 (early-stage or new businesses)

- Kishor — ₹50,001 to ₹5 lakh (growing businesses requiring working capital or asset purchase)

- Tarun — ₹5 lakh to ₹10 lakh (established businesses with documented business history)

For Kishor and Tarun category loans, banks consistently require a detailed project report to evaluate business viability before processing the application.

Mudra loans are classified into three categories:

- Shishu Loan – Up to ₹50,000 (early-stage or new businesses)

- Kishor Loan – ₹50,001 to ₹5 lakh (growing businesses)

- Tarun Loan – ₹5 lakh to ₹10 lakh (established businesses)

For Kishor and Tarun loans, banks usually demand a detailed Mudra Loan project report to evaluate business viability.

Mudra Loan Eligibility — What Banks Actually Check

Eligibility for a Mudra loan is straightforward on paper. The real challenge is demonstrating eligibility through documentation. Banks check:

- Business type: non-corporate, non-farm, micro or small enterprise

- Purpose: productive business activity (not personal or speculative)

- Credit history: CIBIL score and existing loan repayment record

- Business viability: demonstrated through the project report — income projection, expense structure, and repayment capacity

- Promoter background: qualifications, experience, and net worth

Meeting eligibility criteria does not guarantee sanction. A well-prepared project report is what converts eligibility into approval.

What Our Mudra Loan Project Report Covers

- Business Overview and Promoter Profile Clear description of the business activity, the promoter’s background and experience, and the purpose of the loan — structured to address what Mudra-lending bank officers specifically evaluate.

- Market Analysis Who are your customers? What is the local market demand for your product or service? Who are your competitors and how will you acquire customers? Realistic, locally grounded market analysis — not generic national data.

- Technical Plan Equipment or machinery required, raw material sources, production capacity or service delivery model, and manpower requirements. For manufacturing businesses, this section determines whether the loan amount requested is realistic.

- Project Cost and Means of Finance Total investment — working capital, equipment, and setup costs. Breakdown of your own contribution versus the Mudra loan amount requested. Figures must be backed by actual quotations, not estimates.

- 5-Year Financial Projections Projected P&L, Balance Sheet, and Cash Flow for years one through five — all internally consistent and DSCR-verified. Revenue projections are based on realistic capacity utilisation at the local market level — not optimistic assumptions that experienced bank officers immediately question.

- Loan Repayment Schedule Month-by-month repayment plan matched to your bank’s actual lending rate and loan tenure. For new businesses, a moratorium period of 3 to 6 months is typically built in — our repayment schedule accounts for this correctly.

Why You Need a Project Report for a MUDRA Loan

Many applicants believe that Mudra loans are approved only on the basis of eligibility and basic documents. In reality, the project report is the most critical document in the Mudra loan approval process, especially for Kishor and Tarun categories.

Banks need a Mudra Loan Project Report to answer three key questions:

- Is the business viable?

- Can the business generate stable income?

- Will the borrower be able to repay EMIs on time?

Without a proper project report, the bank has no clarity on how the loan amount will be used and recovered.

Why Choose Sharda Associates for Your Mudra Loan Project Report?

Choosing the right consultant can make a significant difference in loan approval outcomes. Sharda Associates offers end-to-end support for Mudra loan applicants.

What Makes Us Different:

- Bank-ready Mudra Loan Project Reports

- Customized DPR as per business type and loan category

- Realistic financial projections accepted by banks

- Experience across Shishu, Kishor, and Tarun loans

- Quick turnaround time

- Support for bank queries and revisions

Our goal is not just documentation, but helping you secure the Mudra loan smoothly.

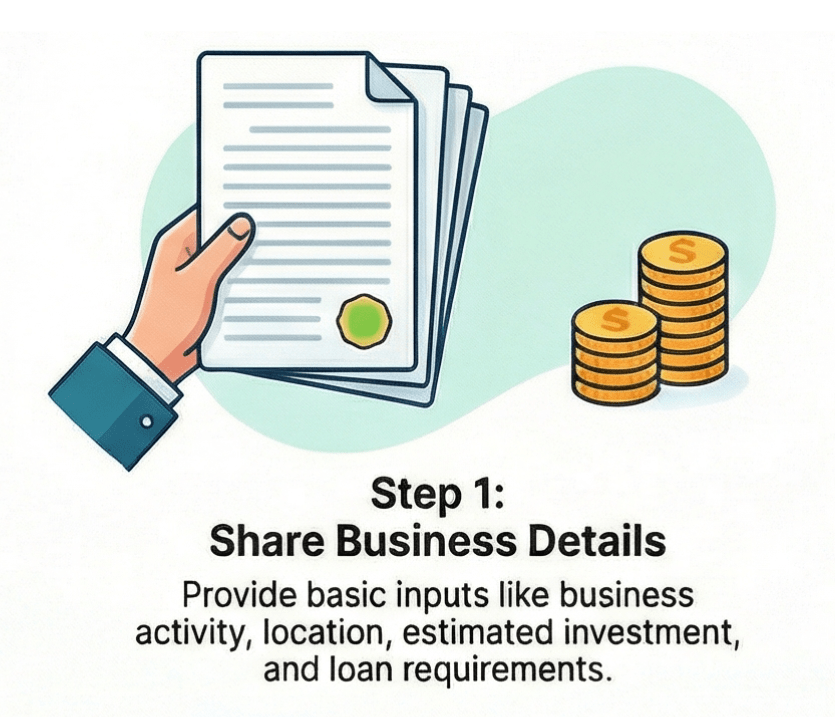

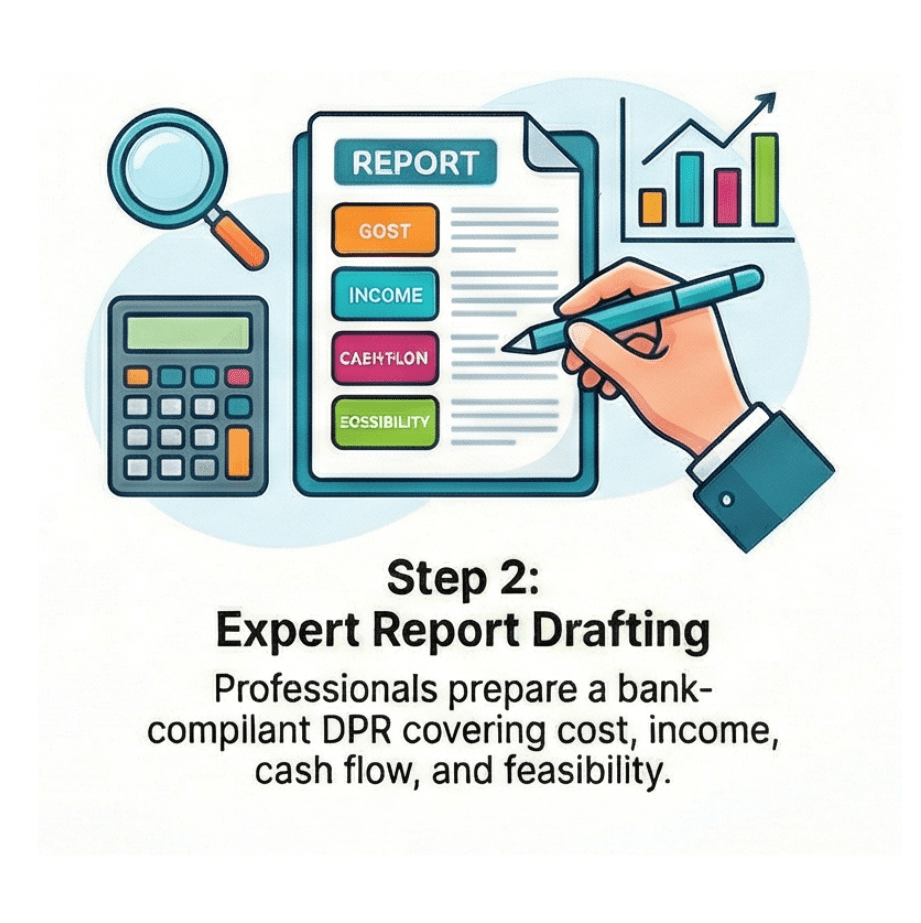

Generate Mudra Loan Project Report in Just 3 Simple Steps

Contents of a Bankable Mudra Loan Project Report

A standard Mudra Loan project report prepared by professionals includes the following sections:

- Executive summary of the project

- Business profile and promoter background

- Nature of business and operational model

- Project cost details (equipment, setup, working capital)

- Means of finance (loan and own contribution)

- Mudra loan category (Shishu/Kishor/Tarun)

- Working capital assessment

- Market analysis and demand potential

- Pricing and revenue model

- Five-year financial projections

- Profit and loss statement

- Cash flow statement

- Break-even analysis

- Repayment capacity assessment

Each section is structured to meet bank credit appraisal standards.

Common Reasons Mudra Loan Applications Are Rejected

Understanding why applications fail is the first step to ensuring yours does not:

- Project report missing or prepared in an incorrect format for the lending bank

- Financial projections that are internally inconsistent (P&L and Balance Sheet do not reconcile)

- DSCR calculation missing or below the 1.25 minimum threshold

- Loan amount requested not matching the stated business plan

- Promoter’s CIBIL score below the bank’s internal threshold

- Business activity not clearly qualifying as non-farm, non-corporate micro enterprise

Our CA team addresses the documentation issues — the ones that account for the majority of Mudra loan rejections — before your file reaches the bank.

Frequently Asked Questions

Some banks do not ask for detailed project report for Shishu category loans (up to Rs 50,000). For the Kishor (up to Rs 5 lakh) and Tarun (up to Rs 10 lakh) categories, a project report is near-mandatory — banks won’t even consider the application without it. We recommend that you have CA certified project report for all three categories.

A Mudra loan project report should include a business overview and promoter profile, market analysis, technical plan (equipment, raw materials, capacity), project cost and means of finance, 5-year financial projections (P&L, Balance Sheet, Cash Flow), DSCR calculation, and a loan repayment schedule matched to your specific bank's lending rate and tenure.

At Sharda Associates, CA-certified Mudra loan project reports start at ₹2,999. Call or WhatsApp +91 89899 77769 for a free consultation and same-day quote. All revisions are free until your loan is approved.

Yes. Overstated or unrealistic income projections are one of the biggest reasons for rejection. Banks prefer conservative and achievable numbers. A professional project report ensures realistic projections aligned with market conditions.

Yes. For existing businesses, banks expect a project report showing current performance, expansion plan, and how the Mudra loan will increase income. Without this clarity, banks may delay or reject the loan.

No. Each scheme has different evaluation criteria. A PMEGP or general business project report cannot be directly used for a Mudra loan. The report must be specifically prepared as per Mudra loan and bank appraisal norms.

A professional report:

- Aligns with bank credit appraisal format

- Uses realistic financial assumptions

- Clearly explains fund utilization

- Demonstrates repayment capacity

This reduces risk perception and increases approval chances.

Sharda Associates not only prepares the Mudra Loan Project Report but also assists in:

- Handling bank queries

- Making revisions if required

- Clarifying financials to bankers

This end-to-end support helps applicants move closer to loan sanction.

At Sharda Associates, your complete CA-certified Mudra loan project report is delivered within 24–48 working hours of payment confirmation — over WhatsApp or email, in PDF and Word format, from our Bhopal office serving all of India.