Tax Collected at Source or TCS is a direct tax imposed on purchasers of certain products by the retailer. TCS is an income tax paid according to the provisions of Article 206C of the Income Tax Act, 1961. TCS shall apply only to the purchasing of certain specified products referred to in the Act.

Example: A, a seller, delivers 10,000 rupees worth of products to B. On the products 1 percent of TCS applies. B must pay 10,000 rupees plus a levy on 100 rupees. The total amount of B has charged is 10100 rupees. A should deposit the Government with the 100 rupees.

Applicability of Tax Collected at Source

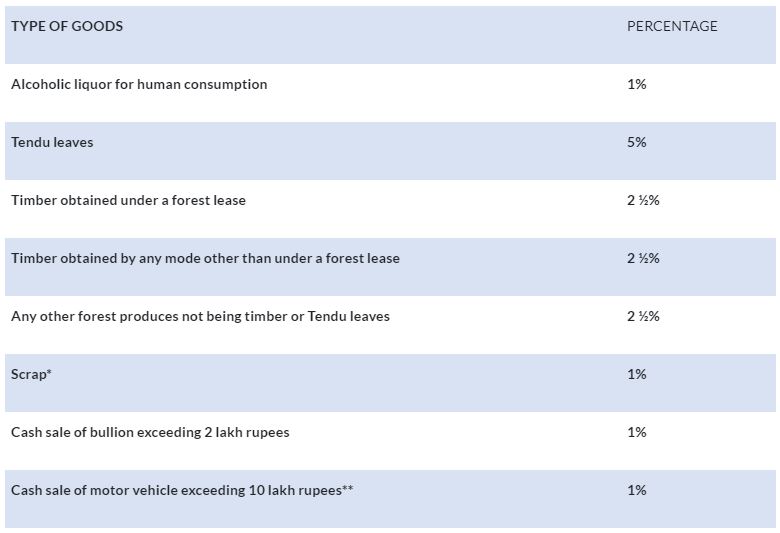

Tax Collected at Source extends only to those products. These goods were listed in the Income Tax Act, 1961, together with the rates at which that tax would apply.

* Scrap contains waste from the manufacture or mechanical process of material that can not be used for breakage, cutting, scratching, or other purposes.

* * The following categories of purchasers are excluded from TCS such as the Central Government, the State Government, the Embassy, the High Commission, the Legation, the Commission, the Consulate and the Commercial Representative of a Foreign State; local authority as specified in the description of clause (20) of Section 10; a public sector company engaged in passenger transport.

TCS shall be applicable where a lease or license is issued. These are the following cases where TCS is applicable when a lease or license is issued.

Who is responsible for paying tax collected at Source?

At the time of purchase of goods, TCS is obtained from the buyer by the seller. For TCS purposes, understanding who qualifies as a buyer and a seller is vitally important.

Buyer:

“Buyer” could include an individual who receives the goods set out in Table 1.1 and Table 1.2 by way of sale, auction, tender or any other such mode for the reasons of Tax Collected at Source. The buyer shall include any person eligible to receive any such goods. As per the Income Tax Act, 1961, purchasers should not include:

- A public sector organization

- The Central Government

- A State Government

- Embassy, High Commission, Legation, Commission, Consulate and a Foreign State Trade Representative

- A club

- A consumer shopping for personal use.

For the intent of Tax Collected at Source, a “seller ” includes:

- The Central Government

- A State Government

- Any local authority or company established by or under central, state or provincial act

- Any business, corporation or cooperative society

- A person or Hindu Undivided Family whose total company or occupational income, gross receipts, or turnover exceeds the monetary limits set out in clause (a) or clause (b) of Section 44AB in the preceding year.

Hire a Professional tax consultant

Exemptions from Tax collected at source

In two situations a buyer may be exempted from TCS.

Lower TCS rate: Where the Assessing Officer is completely comfortable that the purchaser’s total income warrants tax collection at a lower rate than those set out in the Table, the Assessing Officer may issue a tax collection certificate to the purchaser at a lower rate upon application by the purchaser with Form No. 13.

Complete Exemption: The consumer in Form No. 27C law stated that the products are to be used purely for the purpose of manufacturing, processing, or manufacturing articles or objects and not for the purposes of trade.

Process of collection of Tax Collected at source

- TCS can be paid online via the government site, or offline via a bank.

- After subtracting the tax amount at the time of sale, the seller deposits the balance of the TCS with the officials within 7 days of the last day of the month. For example, TCS must be filed on or before 7th February for the month of January. To complete this process the seller must fill out Challan 281.

- Return is filed on or before July 15, October, January, and May on a quarterly basis via Form 27EQ.